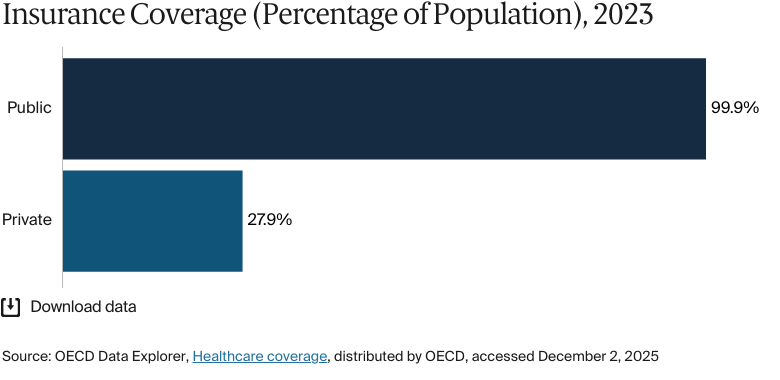

Health insurance is mandatory in Germany, and the health care system offers near-universal coverage, providing access to an extensive range of inpatient and outpatient services. About 99.9 percent of residents are covered by statutory insurance via nongovernmental providers known as sickness funds, which are financed through compulsory wage contributions that are shared equally by employer and employee.

A robust social security system supports coverage for unemployed and low-income individuals. As of 2022, about 27 percent of the population — mostly higher-income individuals; certain professional groups, such as civil servants; and the self-employed — had substitutive private health insurance.1

Germany’s health care expenditure per capita is among the highest in the world, and its health outcomes outperform the regional average. However, digitalization of the health care sector lags behind that of many Western European countries.

In Germany, health insurance is mandatory, with the health care system offers near-universal coverage, providing access to an extensive range of inpatient and outpatient services. German citizens and permanent residents are required to have either statutory health insurance (SHI), consisting of competing not-for-profit, nongovernmental plans known as sickness funds, or private health insurance (PHI).

Public insurance coverage: 100% of population

Private insurance coverage: 27.3% of population

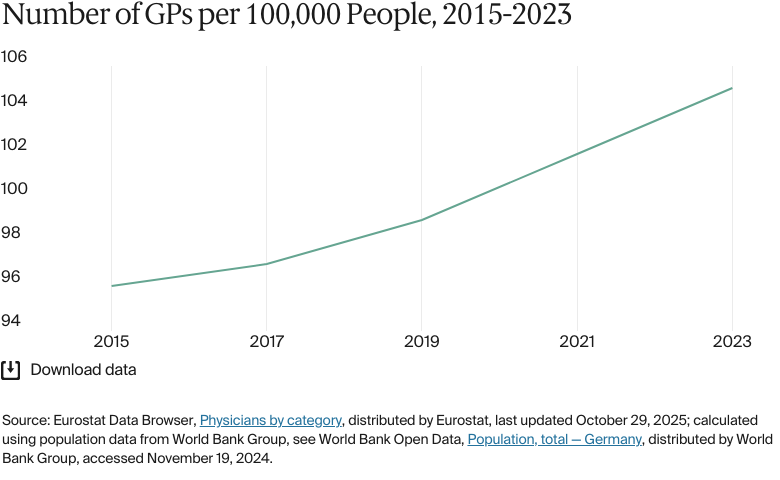

Primary care physicians: 105 per 100,000 people

Specialist physicians: 360 per 100,000 people

Germany’s per capita health expenditure is among the highest in the world. In 2022, total health expenditure was EUR 497.7 billion (USD 538.5 billion); a per capita expenditure of EUR 5,939 (USD 6,426). Total health expenditure in 2023 was EUR 494.6 billion (USD 514.7 billion).

Pharmaceutical spending: 13.7% of total health care budget

Out of pocket spending: 10.7% of total health care spend

In recent years, gaps in life expectancy between socioeconomic groups have widened in recent years. Black men and women, Muslim men and women, Asian women, and White women report experiencing discrimination in the health care system. Data gaps exist for refugees and asylum seekers, and the German migrant population at large.

Additionally, low-income self-employed individuals and those who experience a sudden change in occupation status are at risk populations for health insurance coverage gaps. Addressing mental health remains a major issue for the country overall, but particularly for lower-income groups.

In 1883, Germany became the first country to introduce a national social health insurance system. Initially restricted to industrial workers, coverage was expanded throughout the 20th century and integrated within a more comprehensive social security framework.

Since 2009, all German citizens and permanent residents have been required to have either statutory health insurance (SHI; Gesetzliche Krankenversicherung), consisting of competing not-for-profit, nongovernmental plans known as sickness funds, or private health insurance (PHI). Long-term care is covered under Germany’s mandatory, statutory long-term care insurance (LTCI) (seeLong-Term Care and Social Support).2

The Role of Public Health Insurance

The size of SHI contributions is based on financial capacity. As of December 2023, SHI covered about 89 percent of the population.3

In 2024, SHI was mandatory for all employed citizens with a gross annual income lower than EUR 64,350 (USD 65,174). Nearly everyone has a choice of sickness fund.4

Individuals whose gross wages exceed this threshold, as well as self-employed people previously covered by SHI, can choose to remain in the publicly financed program (about three-quarters opt to do so) or purchase PHI. Civil servants are exempt from SHI; their private insurance costs are partly refunded by their employer. Military personnel, police, and other public-sector employees are covered under programs separate from SHI.5

Sickness funds are mainly financed through compulsory wage contributions — 14.6 percent of gross wages — that are shared equally by the employer and the employee. Dependents (non-earning spouses and children) are covered free of charge. People who are temporarily unemployed contribute in proportion to their unemployment entitlements, while the government contributes on behalf of the long-term unemployed.6

Germans also pay a supplementary income-dependent contribution directly to the sickness fund chosen by each insurer. In 2025, the average supplementary contribution rate that insurance funds charge increased to 2.5 percent. The increase is due to severe financial difficulties that funds are facing from rising health care costs.7

Services Covered by Public Health Insurance

The following services are free of charge for SHI-covered residents:8

Preventive care

Inpatient care (except for follow-up treatments)

Outpatient care

Maternity care

Primary care

Clinically necessary dental care (typically full coverage for those under age 18)

Eye care (means-tested)

Some mental health care

Palliative care

Long-term care (through the mandatory LTCI)

Rehabilitative care

Clinically necessary home visits

Assistive devices (a majority are covered under SHI)

All essential vaccinations and some nonessential and travel vaccinations.

For inpatient preventive care and rehabilitative care, follow-up treatments require a copayment of EUR 10 (USD 11) per day, but this copayment applies for a maximum of 28 days per year, even if the treatment continues beyond that period.9

For dental care, SHI covers the cost of two dental checkups a year for adults and children over age 6. Some preventive treatments are also covered. Other services, such as dental prostheses and fillings, are partially covered.10

For eye care, SHI covers costs only for individuals with severe vision problems and children under age 18.11

Not all SHI providers offer at-home services or visits, but some cover these in certain instances, such as for individuals with a severe illness who are struggling to provide childcare. Inpatient palliative care is covered only for patients who can no longer be cared for at home.12

For mental health care, SHI typically covers outpatient psychotherapy only. Private insurers tend to offer broader coverage.13 Individuals can access free addiction counseling and other treatments under SHI.14

Assistive devices and pharmaceuticals are also subject to copayments. For aids such as wheelchairs or hearing aids, there’s a 10 percent copayment for each aid. For prescription medication, patients are required to pay 10 percent of the drug’s price, with a minimum of EUR 5 (USD 5) and a maximum of EUR 10 (USD 11). Contraception is covered only until age 20.

Modest copayments for hospital stays, prescription drugs, medical aids, dentures, most nonemergency transportation, and certain physiotherapy and medical rehabilitation services are determined by federal legislation and fixed across all sickness funds.15

Safety Nets

Germany has a long tradition of exempting certain population groups from copayments. Among these are children under age 18 (except for dentures, orthodontic treatment, and transportation) and women requiring maternity care. For individuals receiving unemployment or social security benefits, their respective benefits agency usually covers their health insurance contributions.16

A cost-sharing cap applies for all SHI-covered adults; total annual copayments are limited to 2 percent of an individual’s gross annual income. For people with severe chronic illnesses who received the recommended counseling or screenings before becoming ill, the limit is 1 percent.17

The Role of Private Health Insurance

In 2023, more than 8.7 million people (about 11% of the population) were fully covered by substitutive PHI. This level has been fairly stable over the past decade. In addition, 29.6 million SHI-insured individuals (about 36% of the population) had supplementary or complementary PHI coverage, a number that has risen steadily over the past decade. Common top-up benefits include private hospital rooms, more extensive dental services, treatment from specified medical professionals, and SHI copayment coverage.18

Most individuals with substitutive PHI are self-employed, active or retired civil servants, public-sector employees, or people with an annual income above the SHI threshold. Individuals with PHI must also obtain private LTCI.19

Through a fee schedule, the federal government determines provider fees under substitutive, complementary, and supplementary PHI. These fees tend to be higher than SHI fees. All private health insurers are required to offer a basic tariff that provides benefits equivalent to SHI at a premium not exceeding the highest SHI contribution.20

The Role of Government

The structure and governance of the German health care system are more complex and fragmented than in most countries. Decision-making powers are divided among the federal government, the 16 state governments, and self-regulated corporate bodies representing payers (for example, sickness funds), providersand the German Hospital Federation [Deutsche Krankenhausgesellschaft e.V.]). A notable feature is the high level of self-governance delegated to these bodies, which are formally represented in the 13-member Federal Joint Committee (Gemeinsamer Bundesausschuss).21

The Federal Ministry of Health (Bundesministerium für Gesundheit) sets the regulatory framework for health policy, oversees legislative proposals, and supervises self-governing bodies, but it isn’t directly involved in care delivery. The state (and municipal) governments plan hospital capacity, finance infrastructure investment, and supervise public health services and preventive health initiatives. The Federal Joint Committee is the principal decision-making institution for SHI. It determines which services are covered by the sickness funds and sets regulations, guidelines, and quality measures for most aspects of SHI medical, dental, and inpatient care.22

Integration and Care Coordination

Historically, inpatient and outpatient care have been managed and financed separately, with little coordination between hospitals and outpatient providers. However, over the past 20 years, hospitals have expanded their services to include some outpatient care for rare diseases, severe conditions, and highly specialized treatments. Since 2023, hospitals have been allowed to treat inpatients during the day without the need for an overnight stay.

The implementation of hybrid diagnosis-related groups (DRGs) started in 2024. These groups are designed to ensure that payment for specific procedures is the same, whether performed by an inpatient or outpatient specialist.

However, the impact of these initiatives is limited by a lack of incentives to promote integrated care and by the states’ responsibility for hospital planning, which leads to differences in how services are delivered.23

Germany’s Federal Office for Social Security (Bundesamt für Soziale Sicherung) emphasizes the integration of outpatient, inpatient, and rehabilitative care. It aims to provide medical care from a single source and improve cooperation among all health-related services, including psychologists and pharmacies.

Disease management programs are an example of integrated care in action. These programs are designed to coordinate chronic disease treatment throughout a patient’s illness, and as of March 2024, they had enrolled 7.2 million patients.24

Other care coordination programs include Casaplus and Healthy Kinzigtal (Gesundes Kinzigtal). Casaplus is for older adults with multiple chronic conditions who are at high risk of hospital admission. Case managers work with patients and caregivers directly, providing education and support and coordinating care with other providers.25 Healthy Kinzigtal brings together regional health management companies, general practitioners (GPs), and specialists to develop personalized care plans. The program provides patients with access to a range of health and community services to support their care plans and health coaches and doctors to support their lifestyle changes. It also integrates data so that all providers have access to appropriate medical information.26

Operations and Resources

Overview of the Delivery System

The health care system in Germany can be categorized into three groups:

Primary care includes general practice, screening and prevention programs, oral health, pharmacies, some mental health care, and primary eye care services.

Secondary care includes planned or elective care, usually provided in hospitals; urgent and emergency care, including telephone services; ambulance services; after-hours GP services; and mental health care.

Tertiary care includes specialized services that are most often offered in hospitals.

Unlike in many other countries, private health insurers and long-term care insurers use the same health care providers. Hospitals and physicians treat all patients regardless of whether they have SHI or PHI.

Payment mechanisms for providers in Germany vary depending on the service. GPs and specialists, for example, are subject to prearranged price agreements (which are different for SHI and PHI patients) and are usually paid on a fee-for-service basis.27

On the other hand, hospitals are mainly paid for inpatient care services through DRGs. Instead of billing for each service, they receive a predetermined amount based on a patient’s diagnosis and required treatment.28

Psychosomatic and psychiatric services are paid through a flat-rate payment system called PEPP (see Mental Health Care). Services such as outpatient care, dental care, and pharmacist services are generally fee-based.29

Primary Care

Primary and ambulatory health care are largely delivered by private for-profit providers, including GPs or physicians, dentists, pharmacists, psychotherapists, midwives, and allied health professionals. Individuals with SHI can usually choose any doctor for treatment, but certain specialties, such as radiology, need a referral.

GPs are most patients’ first point of contact. They provide preventive care, manage chronic diseases, and refer patients to specialists, but individuals are not required to register with a family physician, and GPs have no official gatekeeping function. Since 2004, sickness funds have been required to offer their members the option of GP-centered care (Hausarztzentrierte Versorgung), which provides patients with a GP who acts as their main health care coordinator. Patients who choose to enroll may receive bonuses or other incentives from their insurers.30

Most patients live within 1.5 km of a GP. In 2023, there were 88,340 GPs in Germany (105 for every 100,000 people).31 GPs and primary care physicians are required to provide out-of-hours care, which is typically organized through GP cooperatives, in which groups of GPs share responsibility for providing care outside regular office hours. These cooperatives are designed to ensure that patients have access to primary care services during evenings, nights, weekends, and holidays.32

Germany’s GP workforce is one of the fastest-aging in Europe: about one in three GPs is age 60 or over. This demographic shift, combined with ongoing recruitment shortfalls, was expected to cause a shortage of about 20,000 GPs in 2025. Rural and underserved areas will be particularly affected.33

There are no data available for the number of GPs practicing publicly versus privately.

Ambulatory primary, specialist, and inpatient care are separated, contributing to fragmented and uncoordinated service provision, especially in the absence of a mandatory gatekeeping system. While interdisciplinary medical care centers have emerged, single-physician (or solo) practices still dominate (see Integration and Care Coordination).34

Under SHI, GPs and specialists are generally reimbursed on a fee-for-service basis according to a uniform fee schedule negotiated between sickness funds and regional physician associations. SHI-contracted ambulatory physicians must be members of these associations, which act as financial intermediaries between physicians and sickness funds and coordinate care requirements within their regions.35

Outpatient/Specialist Care

In 2023, Germany had a total of 428,474 doctors working in outpatient and inpatient care. About 9 percent were employed by public authorities or corporations. Since 2018, the number of private practice doctors has declined by nearly 8 percent.36 As of 2023, there were about 360 specialists for every 100,000 people.37

From 2002 to 2023, the number of outpatient doctors (public and private) increased by 28 percent. As with GPs, the age distribution of doctors shifted toward older age groups, while the number of younger doctors stayed the same. However, the density of doctors has increased.38 With an average of 453 doctors for every 100,000 people in 2021, Germany is among the top countries for outpatient care density; for comparison, there were 376 doctors for every 100,000 people in Europe in 2022.39

In 2023, SHI spent EUR 47 billion (USD 51 billion) on outpatient medical care, excluding medicines, remedies, and aids. This accounted for 15.4 percent of total SHI expenditure, making it the third-largest category after pharmaceuticals.40

Patients usually access secondary care through referrals from their primary care providers (GPs or family doctors). This system ensures that patients receive appropriate specialist care when they need it. Patients with PHI can often bypass the referral system and access specialists directly.41

Reimbursement for outpatient medical treatment for individuals with SHI is based on the uniform assessment standard (Einheitlicher Bewertungsmaßstab). The medical services listed within this framework are covered by SHI as benefits in kind, with no copayment or practice fee needed.

Medical care centers, licensed doctors, and other SHI-participating providers do not directly bill the sickness funds for their services. Instead, the bill is sent to the Association of SHI Physicians (Kassenärztliche Vereinigung), which health insurance companies then pay. The total is based on morbidity-related total remuneration, which is adjusted annually based on changes in the number and health status of insured individuals. New medical services considered particularly beneficial can be reimbursed outside the morbidity-related total remuneration at fixed prices.42

Physician Education and the Workforce

Germany has 43 medical universities: 39 public and four private. Most public universities have free tuition, making them relatively attractive to foreign students. Fees in private institutions range from EUR 12,000 (USD 12,983) to EUR 30,000 (USD 32,459) per year.43 A medical degree takes six years and is followed by a residency. The minimum degree qualifications are determined at the federal level by the Licensing Regulations for Physicians; there are also state laws and individual university requirements. Specialization requirements are regulated and enforced by the medical chambers within each state.44

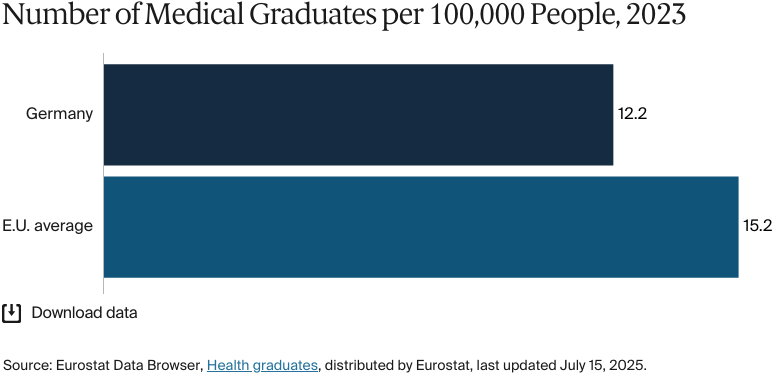

In 2023, Germany had an average of 12.2 medical graduates for every 100,000 people, compared with 15.2 in the European Union (E.U.).45 Although the number of medical students in Germany has increased from 87,863 in 2014 to 108,130 in 2022, the country still struggles with physician shortages.46

In response, Germany recruits medical staff from abroad. As of 2021, foreign-trained doctors accounted for about 13.8 percent of the country’s health care workforce.47 There are no data available for the proportion of the workforce recruited from abroad.

Hospitals

BY THE NUMBERS

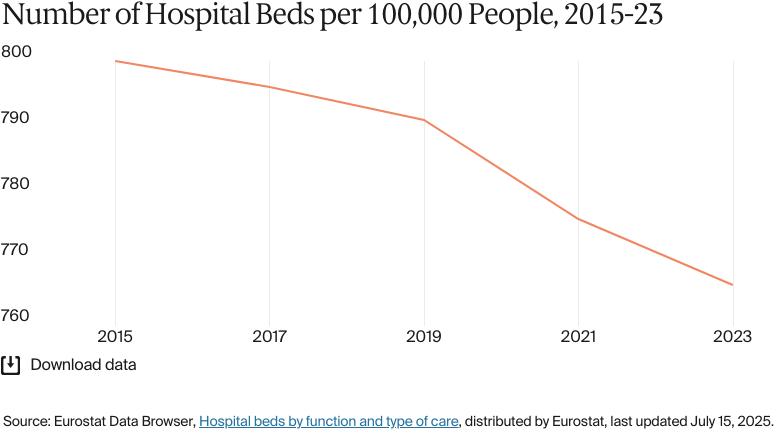

In 2023, Germany had 766 hospital beds per 100,000 people.48

There were 1,225 nurses per 100,000 people in 2023 (compared with an average of 826 in Europe in 2022).49

Germany has a large inpatient sector with high admission rates and one of the highest hospital-bed-to-patient ratios in the E.U. In 2023, there were 766 hospital beds for every 100,000 people, compared with the E.U. average of 511.50 The availability of localized inpatient care was especially beneficial during the COVID-19 pandemic. However, during periods of normal demand for services, this high bed capacity can contribute to inefficiencies and increased funding pressure.51 For example, in 2024, the bed occupancy rate in Germany was 72 percent, implying that almost 30 percent of beds were unused.52 The resources allocated to these unused beds — staff, maintenance, and equipment — drive up running costs without improving patient care.

Hospital funding varies by state. Germany’s states are responsible for capital investment and hospital planning, and some have reduced capital investment over the past 20 years.53 In response, the German Hospital Federation has helped set up a DRG payment system to ensure equitable reimbursement for hospital services (seeOverview of the Delivery System).54

The number of hospitals in Germany has declined over the last three decades. In 1991, there were 2,411 hospitals, but only 1,841 in 2024.55

Germany has one of Europe’s highest densities of nursing and midwifery personnel per capita, at 1,225 nurses and midwives for every 100,000 people.56 Still, the country’s nurse-to-bed ratio is among the lowest in the E.U., partly because hospitals once received a fixed DRG payment for treating specific conditions, regardless of the actual cost. This system meant that hospitals focused on cost efficiency, which led to staffing cuts, including in nursing. Nursing costs were excluded from DRG payments in 2020 to rectify this shortage; by the end of 2025, new laws will require hospitals to meet minimum nursing staff levels (see Health Care Innovation).57

Mental Health Care

BY THE NUMBERS

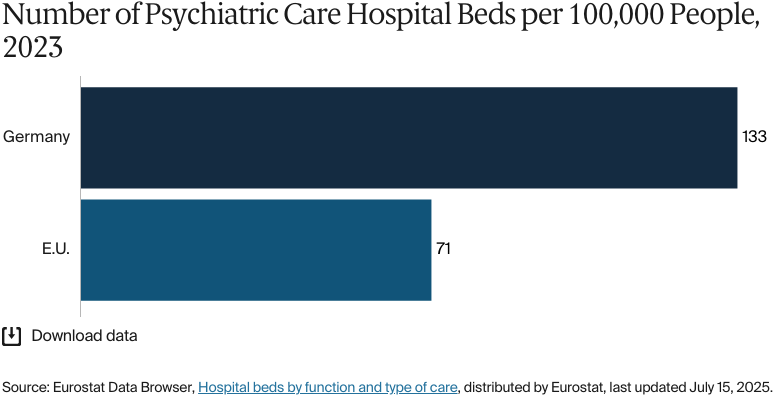

In 2023, there were 133 psychiatric care hospital beds per 100,000 people in Germany, compared with 71 across E.U. countries.58

Germany had 29 psychiatrists per 100,000 people in 2023, much higher than the average of nine in high-income countries in 2020.59

In 2020, the total number of mental health professionals in Germany was 224 per 100,000 people, much higher than the average of 62 in high-income countries.60

As in many countries, Germany is experiencing a rising trend in mental health disorders. In 2021, the prevalence of mental health disorders was 16,051 for every 100,000 people, lower than in France (17,529) and Spain (18,667) but higher than in the U.K. (15,898).61

“One of the challenges is definitely mental health because we see the prevalence of depression and anxiety in Germany increasing over time,” says Dr. Viktoria Steinbeck, research fellow in the Department of Health Care Management at the Berlin University of Technology.

Germany compares favorably with most countries in terms of accessibility [of] health care services, but mental health is an area in which unmet needs of the population are above average. Waiting times for access to ambulatory and inpatient care can be lengthy, with sometimes large regional variations. This isn’t usual for other parts of the German health care system.

Dr. Viktoria Steinbeck

Research Fellow

Department of Health Care Management at the Berlin University of Technology

The overall capacity of mental health facilities is relatively high compared with other high-income countries. In 2020, Germany had 304 mental health hospitals, 331 psychiatric units in general hospitals, 1,259 mental health outpatient facilities, and 81 mental hospital beds for every 100,000 people.62 By 2021, Germany was reporting the highest number of inpatient discharges among individuals treated for mental and behavioral disorders relative to population size: 1,463 discharges for every 100,000 people.63

Individuals with SHI can access licensed psychotherapists without a referral, but primary care providers (such as GPs) can conduct initial assessments and provide referrals to specialists where necessary. These mental health specialists include psychotherapeutic doctors, psychotherapists, and specialized therapists for children and adolescents up to age 21.64

Patients contribute 10 percent of the costs for therapy sessions.65 Providers are reimbursed through the flat-rate PEPP system that replaces the DRG system for these services.66

Long-Term Care and Social Support

Germany has mandatory LTCI for all citizens, with most people getting coverage through their sickness fund (also known as social LTCI) or a private health insurer. Since 1995, statutory sickness fund members (including pensioners and the unemployed) and those with full-cover PHI have been automatically enrolled in LTCI. In 2023, the Social Long-term Care Insurance Act (Pflegeversicherungsgesetz, SGB XI) expanded LTCI services.67 In that year, social LTCI covered about 74.6 million people, and 9.1 million had private coverage.68

Social LTCI benefits are funded mainly by compulsory wage contributions shared equally between the employee and the employer. The standard rate in 2024 was 3.4 percent of gross wages; childless employees age 23 and over paid an additional 0.6 percent.69

As in many other advanced economies, Germany has significantly increased spending on long-term care. In addition to growing demand from an aging population, the rise in spending reflects a series of care provision reforms in the late 2010s. These reforms revised the assessment procedure (establishing a new framework of five care levels), broadened eligibility criteria, and expanded the scope of benefits.70

There are about 1,500 outpatient hospice services, 260 inpatient hospices, and 350 palliative care units in hospitals.71

Cost and Affordability

Health Care Spending Overview

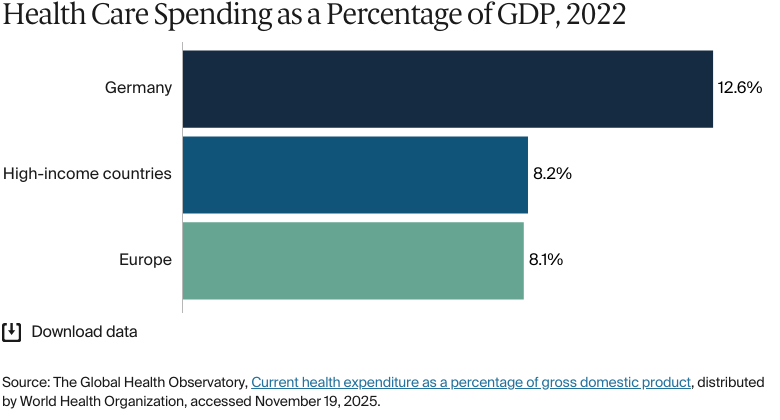

In Germany, as in many high-income countries, health care spending as a share of gross domestic product (GDP) has followed an upward trajectory. In 2024, the ratio was estimated at 12.3 percent, up from 10.8 percent in 2010 and higher than the averages in high-income countries (8.2%) and Europe (8.1%) in 2022.72

In 2022, total health expenditure was EUR 497.7 billion (USD 538.5 billion), a 4.8 percent increase from 2021.73 This equated to a per capita expenditure of EUR 5,939 (USD 6,426). The Federal Statistical Office of Germany (Statistisches Bundesamt) estimated that total health expenditure in 2023 was EUR 494.6 billion (USD 514.7 billion).74

Pharmaceutical Spending

In 2023, Germany’s per capita health care spend on pharmaceuticals was EUR 811 (USD 878), compared with an average of EUR 522 (USD 565) in the E.U. Pharmaceutical spending made up 13.7 percent of all health care spending in that year.75

Drug manufacturers must prove the benefits of a new medicine compared with existing medicines within its first year on the market. Only then will the drug be approved by sickness funds. In that first year, drug manufacturers can set any price for their products; after approval, prices are negotiated with sickness funds. This policy is designed to keep drug prices reasonable while encouraging innovation.

Germany has increased the use of cost-effective generic drugs, and these now have some of the highest volume shares in the E.U. market. A mandatory substitution policy obliges pharmacists to substitute a cheaper generic drug approved by the sickness funds. However, while generic drugs help control costs, rising consumption of all medicines is driving up total SHI spending (seeHow Are Costs Contained?).76

All licensed prescription medicines are generally reimbursable (with cost sharing) under SHI, including new pharmaceuticals that are often expensive (see Primary Care).

Cost Sharing and Out-of-Pocket Spending

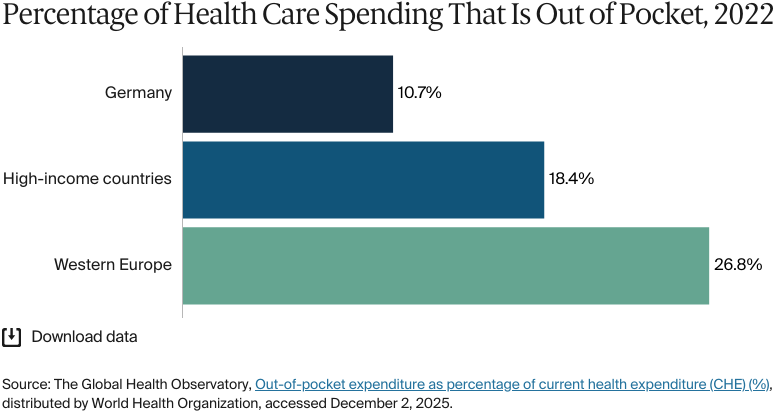

Out-of-pocket spending accounted for 10.7 percent of total health expenditure in 2024, below the E.U. average of 14.9 percent in 2023.77 This reflects the breadth of Germany’s health insurance system coverage.

The largest share of out-of-pocket spending (about 38%) is for long-term care services (seeLong-term Care and Social Support). Pharmaceutical payments are another major expenditure category, accounting for 23 percent of out-of-pocket spending.78

Some services are subject to patient copayments. Copayments are capped — the total is limited to 2 percent of an individual’s gross annual income. For those with chronic conditions, the limit is 1 percent (seeSafety Nets).79

In 2010, 0.02 percent of Germany’s population had been pushed below the poverty line due to household health expenditure.80 These are the latest data available.

How Are Costs Contained?

Cost control has been a prominent part of health care policy because of financial strain across the hospital network, a widening (aggregate) deficit in sickness funds, and higher pharmaceutical and sick pay expenditures.

“Cost containment is an issue, as it is for most social health insurance systems,” says Rudolf Blankart, professor for health care regulation at the University of Bern. “A particular challenge in Germany is the strong allocation of resources tied to the large hospital sector. We have a lot of inpatient facilities that tie up resources that are urgently needed in primary or outpatient care, which is expanding rapidly as technological advances make more treatments possible outside hospitals.”

The Financial Stabilization of Statutory Health Insurance System Act (Gesetzliche Krankenversicherung Finanzstabilisierungsgesetz), which was approved in late 2022, includes measures to contain funding pressures. These include a larger federal grant, an easing of health fund liquidity reserve rules, changes to pricing and reimbursement rules for innovative pharmaceuticals, an extension of the real-terms price moratorium on pharmaceuticals to 2026, and a recommended increase in the supplementary contribution rate paid to sickness funds.81

One of the main objectives of the German Hospital Care Improvement Act (Krankenhausversorgungsverbesserungsgesetz), which came into force in 2024, is to achieve more sustainable financing through reforms to the existing system of flat-rate payments per case (seeHealth Care Innovation).82

Quality and Outcomes

Health Outcomes

BY THE NUMBERS

In 2023, average life expectancy was 80.9 years (compared with 81.1 across high-income countries) — 78.5 years for men and 83.4 years for women.83

The avoidable mortality rate in Germany was 195 per 100,000 people in 2020.84

The top three causes of death in Germany in 2021 were:

Ischemic heart disease: 221 per 100,000 people

COVID-19: 102 per 100,000 people

Trachea, bronchus, lung cancers: 71 per 100,000 people.85

The maternal mortality rate in Germany was four deaths per 100,000 live births in 2023 (compared with 11 on average in Europe).86

The infant mortality rate in Germany was three deaths per 1,000 live births in 2023 (compared with seven on average across Europe).87

In 2021, the share of the German population with mental health disorders was 17 percent (compared with 16% on average in high-income countries).88

In 2023, the suicide rate in Germany was 15 deaths per 100,000 people, lower than the average of 12 per 100,000 people across high-income countries.89

Guns are responsible for one death per 100,000 people in Germany.90

20 percent of adults in Germany were affected by obesity in 2022.91

A major challenge facing Germany’s health care system is increasing demand for health care and long-term care services in an aging population. Workforce shortages are another challenge, especially in rural areas.92

In 2023, average life expectancy in Germany was 81 years, similar to the average for high-income countries (80 years). There was a five-year difference between the average life expectancies of men (78 years) and women (83 years). Between 2010 and 2021, average life expectancy increased by 0.3 years — a smaller rise than in Europe overall (0.7 years).93

Avoidable mortality from preventable and treatable causes was on a downward trend from 2012 to 2020, with rates in Germany consistently below the E.U. average. However, it rose slightly between 2020 and 2022.94 COVID-19 deaths (classified as preventable) increased the avoidable mortality rate in 2021, as they did elsewhere.95

Noncommunicable diseases account for about 90 percent of deaths in Germany. In 2023, cardiovascular disease (34%) was the leading cause of death, followed by cancer (22%) and respiratory diseases (7%).96

Addressing Health Inequities

The share of Germany’s population that reports an unmet need for medical care (0.5% in 2023) is among the lowest in the E.U.97 This suggests that near-universal SHI (or substitutive PHI), combined with extensive outpatient and hospital infrastructure, provides people with good access to health care.

Berlin University of Technology’s Dr Viktoria Steinbeck notes that access to care is not dependent on income. “A key strength of the German health care system is its equitable access to care across income groups. Germany is one of the highest-performing countries in ensuring that low-income individuals are unlikely to face catastrophic spending on health care.”

There are, however, racial and ethnic disparities. In 2023, 38 percent of Black women and 25 percent of Black men said they have experienced discrimination in the health care system. About a third of Muslim men and women said the same, and 61 percent of Asian women said they had been treated less fairly or worse than other people by health professionals. White women also said they felt discriminated against: 30 percent said they didn’t always feel like they were taken seriously by their doctors.98

Refugees and asylum seekers can access maternity, preventive, and emergency care only during their first 36 months in the country. After this period, they are entitled to nearly all SHI services.99

No comprehensive health data exist for Germany’s migrant population. The government doesn’t publish official life expectancy data broken down by race or ethnicity, as it doesn’t collect ethnicity information.100

Coverage gaps in health insurance arise from financial hurdles (for example, changes in employment, self-employment, or low income) or the complex coverage mechanisms of SHI/PHI. Low-income self-employed individuals and those who experience a sudden change in occupational status are two at-risk groups. In 2019, the SHI-Contribution Relief Law (Gesetzliche Krankenversicherung Versichertenentlastungsgesetz) significantly lowered the required minimum SHI contribution (irrespective of income) in an effort to minimize coverage gaps.101

Poor mental health is a considerable issue in Germany, and the lowest-income group experiences some of the highest depression rates in the E.U. In 2019, 21 percent of women in the lowest income quintile reported having depression, compared with 8 percent in the highest income quintile. For men, the rates were 17 and 5 percent, respectively.102

Strategies to reduce health disparities are delegated mainly to public health services, and the levels at which they are carried out vary from state to state. For example, in July 2024, the government approved the creation of a new Federal Institute for Prevention and Education in Medicine (Bundesinstitut für Prävention und Aufklärung in der Medizin) to coordinate and monitor population health status and health-related behaviors, integrate research on noncommunicable diseases, and propose group-specific prevention measures.103

Innovation and Reform

Health Care Innovation

As of September 2024, the government’s principal areas of focus for health care innovation are stabilizing financing across the hospital sector, accelerating digitalization, improving efficiencies and quality of care, and increasing the number of nursing staff.104 These priorities remain in place following the national election in February 2025.

Hospital Innovation

In October 2024, the government approved the Hospital Care Improvement Act, which plans for major reforms of hospital financing and inpatient care, as well as changes to the framework and funding of outpatient services. The intention is to transition from the DRG system of flat-rate fees (per case) to a framework of day-rate payments and grants based on each hospital’s service provision. The government hopes this will reduce economic incentives to overtreat patients and encourage hospitals to shift cases from inpatient to day treatment, thereby improving efficiency and quality of care.105

The Hospital Care Improvement Act came into effect in January 2025 and is being phased in by the end of 2026. However, lack of clarity, concerns over certain aspects of the reform, and tensions between the federal and state governments have created uncertainty about the timeline.106

“Primary care as the main provider of health services is ultimately cheaper and more responsive to people’s needs [than hospitals], but for countries that have traditionally been more dependent on hospital care, it’s not something you can shift to overnight,” says Guillaume Dedet, an Organisation for Economic Co-operation and Development senior health economist. “The journey will take time, but most countries are making the shift to more of a focus on primary care.”

Quality of Care

In parallel with the Hospital Care Improvement Act, in mid-2024, the government approved a draft Health Care Strengthening Act (Gesundheitsversorgungsstärkungsgesetz) to enhance regional outpatient care, improve transparency, and make the family doctor profession more appealing. Some important elements are the removal of longstanding quarterly budget limits for GPs — intended to improve the availability of doctors’ appointments and home visits — and the strengthening of outpatient psychotherapeutic and psychiatric care services for the most at-risk patient groups.107 This act was passed by the Bundesrat in February 2025.108

Nursing Innovation

Nursing staff shortages, a longstanding issue in Germany, have been compounded by more departures from the profession and recruitment difficulties during the COVID-19 pandemic.

Since 2018, there has been a series of reforms to nurses’ training, pay, and working conditions, as well as to the funding model for hospital nursing personnel. Legislation to implement minimum nursing staff levels in hospital wards is being phased in between 2023 and 2025. There are no new federal data to show substantial improvement in recruitment or retention so far (seeHospitals).109

The government has proposed a uniform training standards framework for nursing assistants across Germany. This is set to be implemented by 2027, alongside plans to streamline the way the country recognizes foreign qualifications.110

Health Care Technology

The development of e-health services, including the electronic health card, has been sluggish in Germany, and the quality and scope of services lag behind those available in most of Western Europe.111 Previous reforms, such as 2019’s wide-ranging Digital Healthcare Act (Digitale-Versorgung-Gesetz), targeted nationwide access to an electronic patient record for all SHI-insured people.112 However, implementation has been patchy, and there have been delays and bureaucratic hurdles.

In Germany, like elsewhere, the use of telemedicine increased during the COVID-19 pandemic. Still, the availability and use of remote consultations are modest compared with those in other European countries.113 “Germany’s telemedicine infrastructure is poor. Things are overcomplicated and thought through in so much detail that they’re outdated by the time they’re implemented,” says Dr Viktoria Steinbeck.

The pandemic also propelled Germany’s digital health efforts, prompting the reforms outlined in the 2021 Digital Supply and Care Modernization Act (Digitale-Versorgung-und-Pflege-Modernisierungs-Gesetz). There was also about EUR 4 billion (USD 4.2 billion) of expanded E.U. funding available under the Recovery and Resilience Facility for digital health infrastructure projects and hospital modernization.114

Two new domestic laws enacted in March 2024 — the Digital Act and the Health Data Use Act (Gesundheitsdatennutzungsgesetz) — are intended to accelerate the rollout and uptake of online consultations, implement a nationwide system of e-prescriptions, and, from 2025, fully implement electronic patient records for all SHI-insured people.115

This content was produced by FT Longitude, the specialist research and content marketing division of the Financial Times Group, on behalf of the Commonwealth Fund. Research and content for the Commonwealth Fund country profiles were collected by FT Longitude between February and December 2025.

This profile reflects data as of January 2026. New or updated information may have become available since its release.

“Addiction help” (Suchthilfe), German Centre for Addiction (Deutsche Hauptstelle für Suchtfragen e. V.), accessed December 20, 2024, https://www.dhs.de/suchthilfe.

↩

Caroline Berchet and Carol Nader, “The organisation of out-of-hours primary care in OECD countries," OECD Health Working Papers, no. 89, September 21, 2016, https://doi.org/10.1787/5jlr3czbqw23-en.

↩

33

Julian Wangler and Michael Jansky, “How can primary care be secured in the long term? – a qualitative study from the perspective of general practitioners in Germany,” European Journal of General Practice 29, no. 1 (June 30, 2023), https://www.tandfonline.com/doi/full/10.1080/13814788.2023.2223928.

↩

“Remuneration for outpatient medical treatments (contract physicians)” (Vergütung Ambulanter Ärztlicher Behandlungen), Federal Ministry of Health (Bundesministerium für Gesundheit), accessed January 13, 2025, https://www.bundesgesundheitsministerium.de/aerztliche-verguetung.html; Association of Substitute Health Insurance Funds, “Doctors – care and contracts.”

↩

“Figures on hospice and palliative care” (Zahlen zur Hospiz- und Palliativarbeit), German Hospice and Palliative Association (Deutscher Hospiz- und PalliativVerband e.V.), accessed September 23, 2024, https://www.dhpv.de/zahlen_daten_fakten.html.

↩

72

The Global Health Observatory, Current health expenditure.

↩

Austin E Schumacher et al., “Global age-sex-specific all-cause mortality and life expectancy estimates for 204 countries and territories and 660 subnational locations, 1950–2023: a demographic analysis for the Global Burden of Disease Study 2023.” The Lancet 406, no. 10513 (October 18, 2025):1731–1810, https://doi.org/10.1016/S0140-6736(25)01330-3.

↩

Institute for Health Metrics and Evaluation, GBD compare, distributed by IHME, accessed November 27, 2025, https://vizhub.healthdata.org/gbd-compare/; overall firearm mortality is the aggregate of physical violence by firearm, self-harm by firearm, and unintentional injuries by firearm.

↩

91

World Health Organization, Age-standardized prevalence of obesity among adults (18+ years), distributed by WHO Data, last updated February 29, 2024, https://data.who.int/indicators/i/C6262EC/BEFA58B.

↩

“Correction: Death Statistics 2023: Number of Deaths in 2023 Decreased by 3.6%” (KORREKTUR: Todesursachenstatistik 2023: Zahl der Todesfälle im Jahr 2023 um 3,6 % Gesunken) (Press Release, Federal Statistical Office of Germany [Statistisches Bundesamt], September 30, 2024), https://www.destatis.de/DE/Presse/Pressemitteilungen/2024/08/PD24_317_23211.html.

↩

Explore how countries compare on key health system characteristics including health care coverage and spending, the health workforce, health outcomes, and more.