Health costs in 2026 are projected to grow at a faster pace than in recent years for the third year in a row, driven by hospital consolidation that increases the price of medical services; ongoing hospital labor shortages; overall inflation in the cost of supplies, GLP-1 drugs, and other specialty medications; and increased use of behavioral health services. Consumers see the effects of these increases in what they pay toward their premiums and in how much they pay when they go to the doctor, fill a prescription, or have surgery.

Most people under age 65, about 167 million people, get their health insurance through an employer or a family member’s employer, and share the cost of the premium with their employer. Employers pay on average around 70 percent of the cost of total premiums for family coverage. Employees pay the remaining portion, called a premium contribution, along with other costs like deductibles and copayments. Family coverage premiums averaged $24,540 in 2024, with employees contributing $7,216 annually.

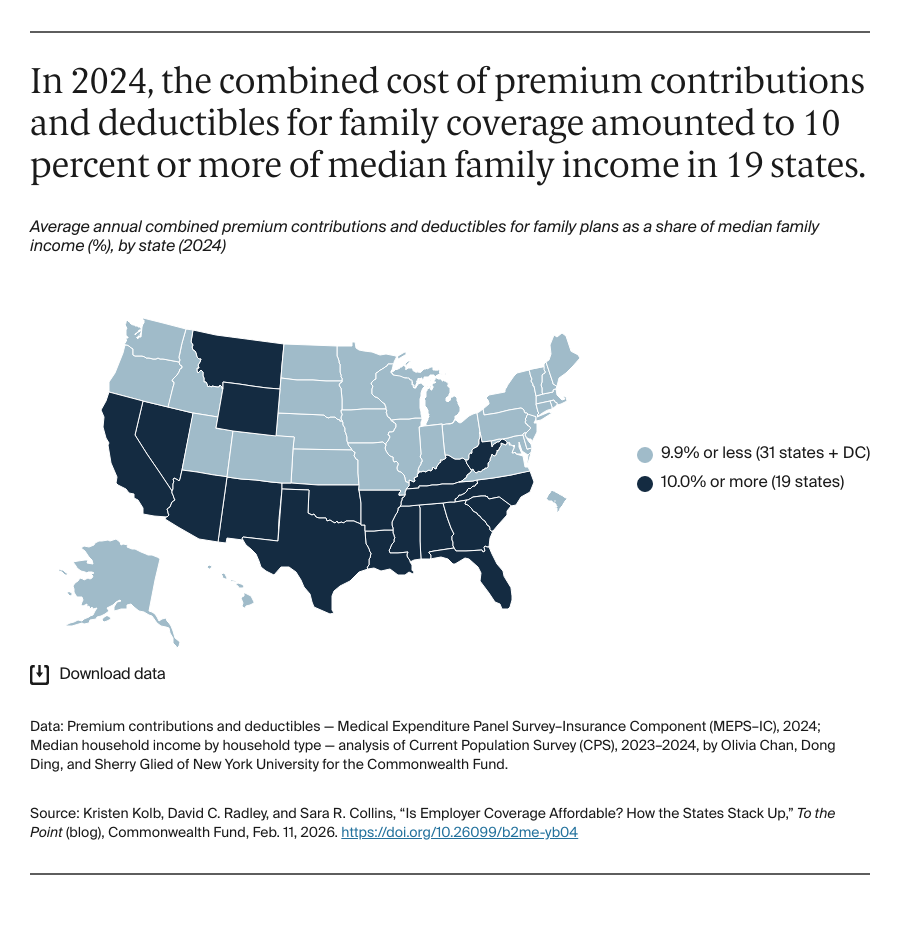

Given the increases in costs, how affordable is employer coverage for the 63 percent of working-age adults who get their coverage this way? To assess affordability, we looked at the most recent available national data from 2024 on what employees paid for premiums and deductibles in all 50 states and the District of Columbia compared to state median income. We found that the share of income spent on premium contributions and deductibles together for family coverage ranged from a high of 15.6 percent in Louisiana to a low of 5.7 percent in the District of Columbia. Generally, employees in states with lower median incomes spent a relatively larger share of their income on these costs than those living in states with higher median incomes. If incomes don’t keep pace with the increase in health care costs over the next few years, paying for employer coverage and getting health care could consume increasingly higher shares of people’s incomes.